For seniors, dental insurance holds significant value, as it provides both financial relief and access to much-needed care. As individuals age, they often face increased dental needs, from gum disease to tooth loss, necessitating frequent visits to the dentist.

Without dental insurance, the cost of these visits and treatments can quickly become overwhelming. Insurance plans for seniors often prioritize services that address common age-related dental issues, ensuring individuals can maintain oral health without depleting their savings.

Dental insurance offers an array of benefits that specifically target the needs of older adults. Preventive services, such as cleanings and check-ups, are typically covered with minimal or no out-of-pocket expense, encouraging regular care.

This proactive approach helps detect dental issues early, significantly reducing the need for more invasive and costly procedures later. When more complex treatments are needed, such as fillings, crowns, or even dentures, insurance can help offset these expenses, offering a layer of protection against sudden, large fees.

Another critical aspect of dental insurance for seniors is the peace of mind it provides. Understanding what insurance plans cover, including any pre-existing conditions and limitations, helps seniors plan ahead and budget effectively.

By choosing an appropriate insurance policy, they can ensure access to necessary services, which is reassuring for both the individuals and their caregivers. Dental insurance can also facilitate continuity of care, allowing seniors to maintain their relationship with trusted healthcare providers within the network, maximizing both comfort and care quality.

Ultimately, the savings provided by dental insurance contribute to a more stable financial situation, enabling seniors to allocate funds to other important areas, like medications or routine healthcare needs.

Striking the right balance between coverage and cost is essential, and understanding the various aspects of dental insurance makes it easier to find a policy that supports long-term oral health for seniors, enhancing their quality of life.

To further illustrate the advantages of dental insurance for seniors, consider these key points about what to look for when selecting a plan:

- Check coverage for routine cleanings and preventive care to maintain oral health.

- Ensure the plan includes coverage for restorative treatments like crowns and dentures.

- Assess the network of dentists and the availability of specialists.

- Review out-of-pocket costs, including deductibles and co-pays, for transparency.

- Consider additional benefits, such as discounts on vision or hearing services.

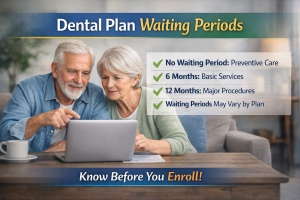

- Confirm the policy’s terms on pre-existing conditions and waiting periods.

- Analyze the stability and reputation of the insurance provider.

These considerations can help seniors make informed decisions about dental insurance, enhancing their well-being.